SDE and EBITDA are two different ways of measuring the profit or cash flow of a business.

The main difference between SDE and EBITDA is:

SDE – The primary measure of cash flow used to value small businesses and includes the owner’s compensation as an adjustment.

EBITDA – The primary measure of cash flow used to value mid to large-sized businesses and does not include the owner’s salary as an adjustment.

Adjustments

Numerous adjustments are made when calculating both SDE and EBITDA. For example, interest, taxes, depreciation, and amortization are added back when calculating both SDE and EBITDA, and many of these adjustments are similar in both methods. The major difference is that SDE includes the owner’s compensation, and EBITDA does not include the owner’s compensation.

The Purpose of Calculating SDE and EBITDA

The purpose of calculating SDE and EBITDA is so businesses can be compared to one another on an apples-to-apples basis. To make a uniform comparison, the adjustments for both should be consistently applied.

Before you begin selling your business, you’ll need an effective valuation. To reach this, you’ll use SDE (seller’s discretionary earnings) or EBITDA (earnings before interest, taxes, depreciation, and amortization). But what’s the difference between SDE and EBITDA?

Let’s explore both valuation options in-depth and unpack some of the major (and not so-major) differences you may encounter at this stage of the M&A process.

When To Use SDE

Definition

Seller’s discretionary earnings, or SDE, is defined by the International Business Brokers Association (IBBA) as:

Net income, plus

Interest expense or income (the “I” in EBITDA), plus

Taxes (income taxes, the “T” in EBITDA), plus

Depreciation and amortization (the “D” and “A” in EBITDA), plus

Non-recurring income and expenses, plus

Non-operating income and expenses, plus

Owner’s total compensation for one owner, after adjusting the compensation of all other owners to market value.

When is SDE used?

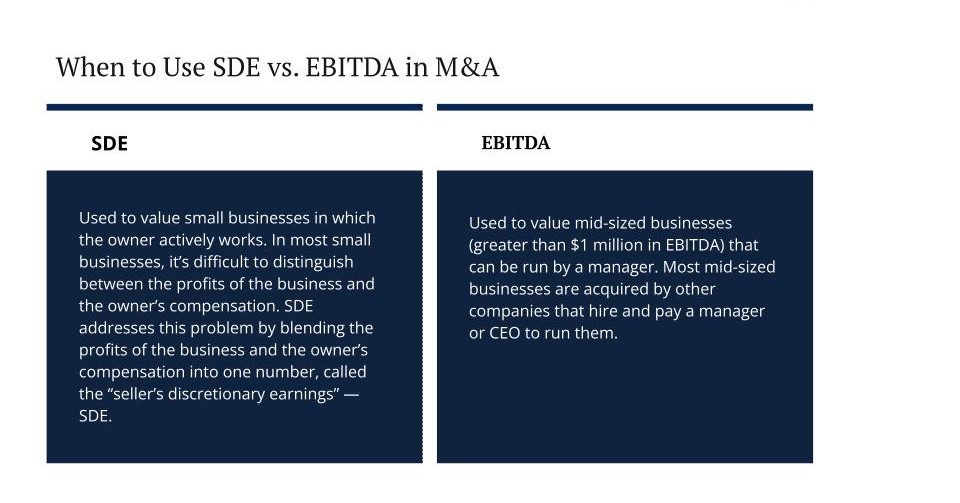

SDE is used to value small businesses in which the owner actively works.

Why is SDE used?

In most small businesses, it’s difficult to distinguish between the profits of the business and the owner’s compensation. Many owners don’t pay themselves a salary but may take a “draw.” In others, an owner may pay themselves less than they would to an outside manager.

For example, the owner may pay themselves a $75,000 annual salary when a more appropriate salary for their role, based on market demand, would be $150,000 per year.

Additionally, many small business owners deduct numerous personal expenses (“perks”) through the business that wouldn’t be paid to a manager in the same position. Often, distinguishing between profits and compensation isn’t practical since most blur the line between “business” and “personal.”

For example, a business may be paying for an owner’s personal vehicle, health club membership, vacation home, and personal travel expenses.

SDE addresses this problem by blending the profits of the business and the owner’s compensation into one number, called the “seller’s discretionary earnings” – SDE. This is the total compensation that’d be available to a new owner-operator of the business, regardless of how they characterized the income – whether as perks, a salary, a draw, or dividends.

The smaller the business, the harder it is to separate “business” from “personal” profits and perks. SDE addresses this by blending them together into “seller’s discretionary earnings.”

What size businesses use SDE?

SDE is normally used with businesses that have less than $1 million in SDE. Business brokers mainly use the SDE calculation since they tend to sell businesses run by an owner-operator.

When To Use EBITDA

Definition of EBITDA

EBITDA is defined as Earnings (E) Before (B):

Interest (I)

Taxes (T)

Depreciation (D)

Amortization (A)

When is EBITDA used?

EBITDA is used to value mid-sized businesseswith greater than $1 million in EBITDA. This is because the majority of companies in the middle market are purchased by other companies that must hire and pay a manager or CEO to run them post-closing.

When is the owner’s salary normalized?

If an owner-operator currently runs the business, the owner’s compensation is normalized to market levels.

For example, if the owner’s current salary is $500,000 per year, and the market rate is $200,000 per year, then the owner’s compensation is normalized to $200,000 per year.

If the current owner isn’t paid a salary, then an appropriate market rate is deducted when calculating EBITDA. The same is true if the current owner or manager is underpaid. Regardless of what the current owner pays themselves, their compensation is normalized to current market levels for a manager or CEO, which averages from $150,000 to $300,000 for most businesses in the lower-middle market.

Why is a manager’s salary deducted?

If a private equity firm or other corporate buyer acquired a business, they would need to hire a manager to run it, which is why the owner’s compensation is not added back. In a small business, an owner would keep the owner’s compensation, but in a mid-sized business, the new owner would need to pay a manager to run the business.

For example, if the SDE is $1,000,000, and a competitor bought the business and paid a manager $200,000 per year to run it, their EBITDA would be $800,000 per year ($1,000,000 – $200,000 = $800,000).

What size businesses use EBITDA?

EBITDA is normally used when valuing mid-sized businesses that have more than $1 million in EBITDA. It is mainly used by M&A advisors and investment bankers who specialize in selling businesses to private equity firms, competitors, and other institutional buyers.

Most mid-sized businesses are acquired by other companies. EBITDA removes an owner’s salary from the valuation because the buyer will need to spend this figure on a new manager or CEO.

EBITDA is also used as a metric for public companies, but earnings, or simply net income, is more commonly used by publicly held companies.

EBITDA vs. Adjusted EBITDA

The term EBITDA is used loosely and sometimes refers to “adjusted EBITDA.” Adjusted EBITDA includes additional adjustments that aren’t included in the calculation, similar to adjustments that are made to calculate SDE.

When discussing EBITDA, you should clarify if you’re referring to EBITDA or adjusted EBITDA – most M&A advisors are referring to the latter.

Some adjustments included in adjusted EBITDA but not standard EBITDA include:

Non-operating income or expenses

Non-recurring income or expenses

Unrealized gains or losses

Owner perks

SDE vs. EBITDA

Here’s a chart summarizing the differences between SDE, EBITDA, and adjusted EBITDA:

Differences Between SDE, EBITDA, and Adjusted EBITDA

In the example above, if the multiples for the business were the same, it would seem to make sense to always value the business based on SDE because this would result in the highest value. Unfortunately, this isn’t the case.

Why EBITDA Multiples Are Higher

Multiples of EBITDA are higher than multiples of SDE for the simple reason that a business that’s run by a manager should sell for more than one in which the owner is working full-time. For the same price, would you rather buy a business in which you have to work 40 hours per week or one that’s run by a management team and doesn’t require any time commitment from you?

When It’s Not Clear Whether To Use SDE or EBITDA

If the business is on the line, and either SDE or EBITDA could be used to value the business, the choice doesn’t usually impact value significantly.

Here’s an example from a business using both SDE and EBITDA:

$1,000,000 SDE x 3.0 multiple = $3,000,000 asking price

$750,000 EBITDA x 4.0 multiple = $3,000,000 asking price

In this example, I assumed an owner’s compensation of $250,000 per year. This resulted in SDE of $1,000,000 and EBITDA of $750,000 ($1,000,000 – $250,000 = $750,000). As you see, the value I arrived at was identical for both methods.

Let’s examine one final scenario that shows the difference between the multiple applied to EBITDA vs. SDE.

The math doesn’t always work out this well, but this example illustrates that value is often similar regardless of whether you use SDE or EBITDA.

EBITDA Multiples Usually Include Working Capital

What if the value based on SDE is higher than the value based on a multiple of EBITDA? Again, it might seem to make sense to value the business based on a multiple of SDE. Still, businesses sold based on a multiple of EBITDA usually include working capital (inventory, accounts receivable, and assumption of accounts payable) in the purchase price.

Conclusion

Even where the resulting value is roughly the same, SDE and EBITDA are important and verifiable values that allow you to proceed with your M&A advisor on formal and realistic terms.

When valuing a business with less than $1 million in earnings, use SDE, where the owner’s compensation is included. When valuing a business with more than $1 million in earnings, use EBITDA, where the owner’s compensation is excluded.

Keep in mind that the two measures of cash flow concerning owner’s compensation represent the main difference between SDE and EBITDA.

Purchase Price

Custom Package

Standard Package

$1,000,000

$80,000

$120,000

$2,000,000

$160,000

$220,000

$3,000,000

$240,000

$300,000

$4,000,000

$260,000

$360,000

$5,000,000

$280,000

$410,000

$6,000,000

$300,000

$450,000

$7,000,000

$320,000

$480,000

$8,000,000

$340,000

$510,000

$9,000,000

$360,000

$540,000

$10,000,000

$380,000

$570,000

$20,000,000

$580,000

$770,000

$30,000,000

$730,000

$970,000

$40,000,000

$805,000

$1,120,000

$50,000,000

$880,000

$1,220,000

$60,000,000

$930,000

$1,320,000

$70,000,000

$980,000

$1,420,000

$80,000,000

$1,030,000

$1,520,000

$90,000,000

$1,080,000

$1,620,000

$100,000,000

$1,130,000

$1,720,000

Download Your FREE PDF Copy: Food and Beverage M&A